Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

Strong numbers, weak fundamentals—can India truly become a global dairy exporter?

India is not constrained by production—but by product strategy, price competitiveness, and export architecture.

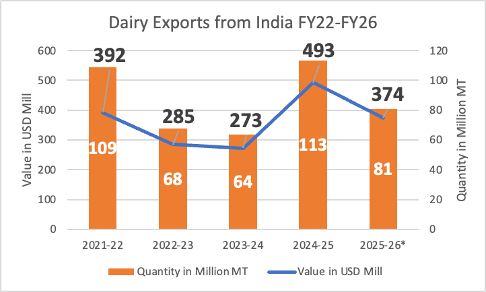

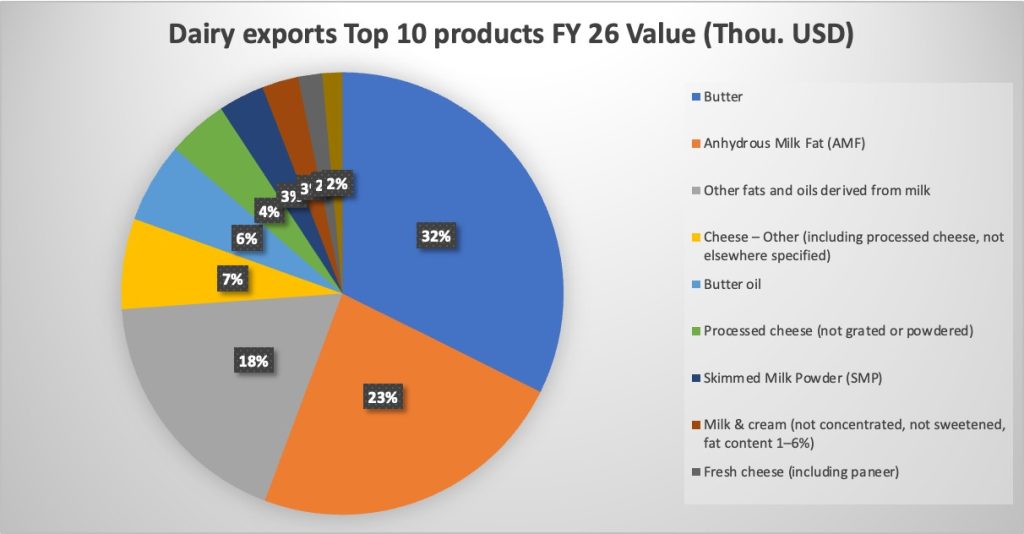

Indian dairy exports are entering a critical inflection point. Despite being the world’s largest milk producer, India’s presence in global dairy trade remains limited, concentrated, and structurally weak, with most categories holding less than 0.5% market share. Export growth over the last few years has been uneven and heavily skewed towards a few segments, particularly milk fats, rather than being driven by a diversified and strategic product mix.

At the same time, global dairy markets are becoming increasingly volatile, shaped by price fluctuations, shifting demand patterns, and geopolitical disruptions. This is creating new windows of opportunity, but also raising the bar for competitiveness in terms of quality, consistency, and product positioning.

“For India, FY26 represents a rare convergence of surplus availability and global demand opportunity, further amplified by disruptions arising from the ongoing US–Iran conflict, which is reshaping trade flows, increasing price volatility, and tightening global supply chains. However, the key question is whether this moment will translate into a strategic expansion of exports, or remain another cycle of opportunistic surplus disposal.”India’s Export Reality: What the Data Really Says

An analysis of the last five years of export data clearly indicates that India exports when it has excess—not when it has a strategy.

A significant portion of export growth in the last 2–3 years has been driven by butter fat realisation, which in turn has even led to domestic shortages of butter fat at the beginning of FY26 (April 2025). This reinforces the structural pattern that exports are opportunistic, not planned.

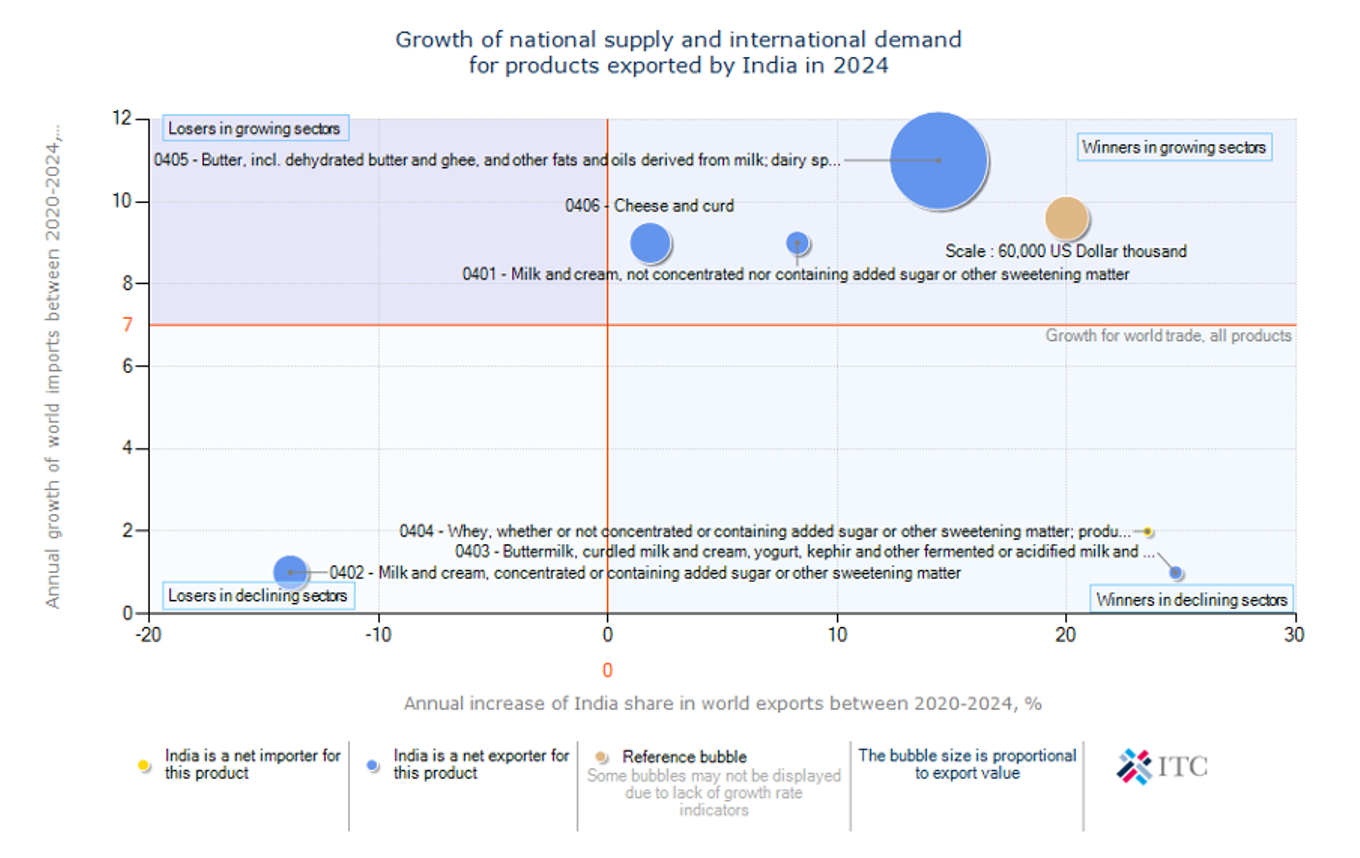

India is exporting dairy—but not exporting value.India’s dairy export profile demonstrates a highly uneven but strategically revealing trajectory. It is strongest in large, fast-growing commodity markets, yet significantly underrepresented in high-growth value-added segments.

Butter and ghee remain the core strength, firmly positioned in a high-growth global market (11%) with strong gains in share (+10–12%). However, even here, India’s 2.4% share reflects low global penetration, indicating that it is still a marginal player despite momentum.

In contrast, cheese (0.2–0.3% share, 9% growth) and liquid milk (0.2% share, 9% growth) highlight missed opportunities, where India is present but not meaningfully participating in global expansion.

The situation is more concerning in SMP (0.2–0.3% share, 1% growth, –10% share decline), where India is losing ground in a stagnant market, and in whey (0.1% share, 2% growth), where it is absent in a future-facing, high-value segment.

From a quadrant perspective:

India’s export basket is aligned with volume, not value. The concentration of 94–96% exports in a few categories is not just a statistic—it is a structural risk.

A closer look at India’s global positioning reveals a deeper structural issue—not just where India stands, but where it is failing to move. India’s export profile clearly shows that it is strong in large, growing commodity markets, particularly milk fats, but underrepresented in high-growth value-added segments.

Butter and ghee remain the only true global success story, with strong demand growth (11%) and the highest market share (2.4%). However, even this success is limited in scale.

Meanwhile:

India is performing well where the world is growing—but still remains a marginal player.India’s dairy export basket is fundamentally misaligned with global demand trends—strong in fats, absent in proteins, and weak in value-added categories.

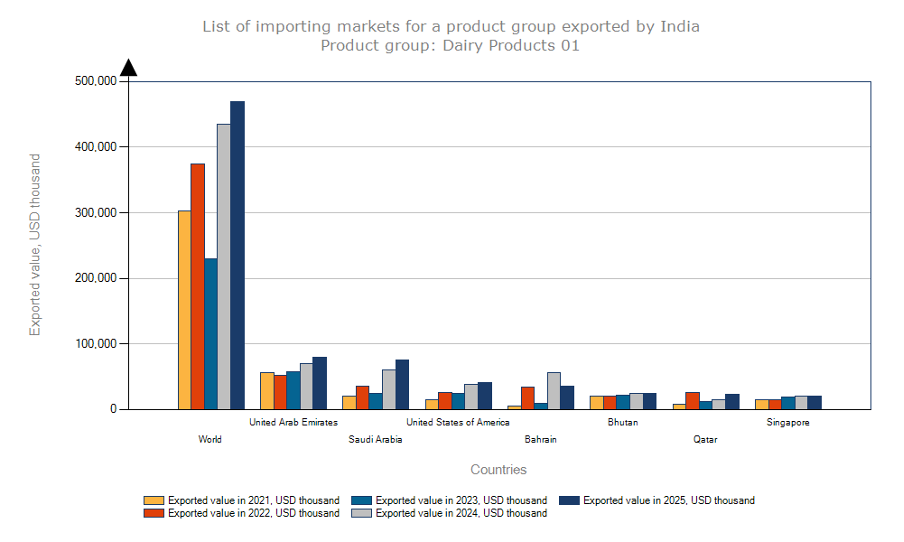

India’s export geography further reinforces this structural imbalance.

These are high-value diaspora-driven markets, where products like ghee, paneer, and traditional dairy command a premium due to cultural affinity. These markets provide stable demand and moderate value realisation.

A premium but niche market, driven by demand for A2 ghee, organic dairy, and protein products. While volumes are small, the value potential is very high, and presence here enhances global credibility.

These offer logistical advantages and stability, but are limited in scale.

India is exporting to markets that buy dairy—but not necessarily to markets that pay for dairy.

The most striking reality is the disproportionately small scale of India’s exports.

In absolute terms:

This is not a gap—it is a structural disconnect.

India may be the world’s largest milk producer, but in global dairy trade, it remains a marginal player.

India’s dairy export story sits at a critical intersection of opportunity and illusion. On one hand, there is a clear opportunity driven by strong global demand in select categories, particularly in milk fats, where India has already demonstrated traction. This is further supported by India’s inherent scale advantage as the world’s largest milk producer, along with an emerging presence in segments like butter, ghee, and select value-added products, indicating that the country has the foundational capability to expand its global footprint.

However, this opportunity is tempered by structural realities that create an equally strong illusion. India continues to operate with low market share across most product categories, largely remaining below 0.5% globally, except in a few cases. Its absence in high-value and protein-led segments, such as whey and functional dairy ingredients, highlights a critical gap in product strategy. Moreover, export growth has historically been driven by surplus availability rather than a consistent, market-oriented strategy, making it cyclical and opportunistic. This is further compounded by weak integration into global value chains, limiting India’s ability to compete with established export-oriented dairy economies.

In essence, while the opportunity is real, the illusion lies in overestimating India’s readiness—without addressing these structural gaps, the export story risks remaining episodic rather than transformational.

If India has to transition from a surplus-driven exporter to a strategy-led global player, the answer lies in region-specific export clusters aligned with product strengths. The country already has natural advantages across geographies—what is missing is integration, standardisation, and export orientation.

A few clear cluster opportunities emerge:

India does not just have the opportunity to export dairy products—it has the capability to export the entire dairy ecosystem.

However, this will require:

India’s dairy export story is not constrained by demand—but by direction. While the country continues to gain in milk fats, it remains largely absent from protein-led, value-added, and future-facing segments that are shaping global dairy trade.

India is exporting dairy—but not exporting value.

Source : Editorial by Kuldeep Sharma Chief editor Dairynews7x7 April 14th 2026

Data Source : ITC, APEDA, Indian Customs, Suruchi research