he latest Global Dairy Trade auction (Event 404 held on May 19, 2026) reflects a dairy market that is steadily moving towards balance, with powders continuing to support the index while milk fats and cheese remain under pressure. The auction confirms that the market leadership has now shifted away from the aggressive fat rally seen earlier this year and is gradually moving towards powder-led stability driven by broader import demand. According to the official Global Dairy Trade results, Whole Milk Powder (WMP) increased by 1.2% to USD 3,772/MT, while Skim Milk Powder (SMP) edged up by 0.2% to USD 3,552/MT, showing that core powder demand remains resilient despite cautious buying behaviour.

The latest product-wise movements clearly show a divergence between powders and fats. Butter increased by 2.5% to USD 5,674/MT after weakness in the previous event, suggesting that some buyers returned to the market at corrected price levels. Mozzarella also strengthened by 2.9% to USD 4,127/MT, while Lactose gained marginally by 0.5% to USD 1,529/MT. However, the pressure continued in the high-fat segment as Anhydrous Milk Fat (AMF) declined by 1.6% to USD 6,344/MT and Cheddar fell by 1.3% to USD 4,560/MT. Butter Milk Powder (BMP) remained unavailable in this event, indicating limited offering or insufficient market determination. These movements indicate that the market is no longer rewarding fats indiscriminately and buyers are becoming more selective in their procurement strategies.

The most important signal emerging from Event 404 is that global demand is becoming more diversified and stable. Earlier, the market was highly dependent on China for directional momentum, but now buying interest is increasingly spread across Southeast Asia, the Middle East, North Africa and parts of Africa. WMP and SMP continue to attract demand due to restocking requirements and improving confidence among importers. China remains active but tactical, purchasing closer to consumption needs rather than building aggressive inventories. This shift is making the global market less volatile and more structurally balanced.

From the perspective of developed dairy economies such as New Zealand, Europe and the United States, the latest auction suggests that milk fat markets are entering a correction and consolidation phase after the sharp rally witnessed during January and February this year. The initial rally in 2026 was driven by tight milk availability, weather-related supply concerns and strong fat demand. However, improving milk flows in Europe and Oceania, combined with softer foodservice demand, are now limiting upside in butterfat-heavy commodities. Cheese markets also remain under pressure because of competitive export supplies from Western producers.

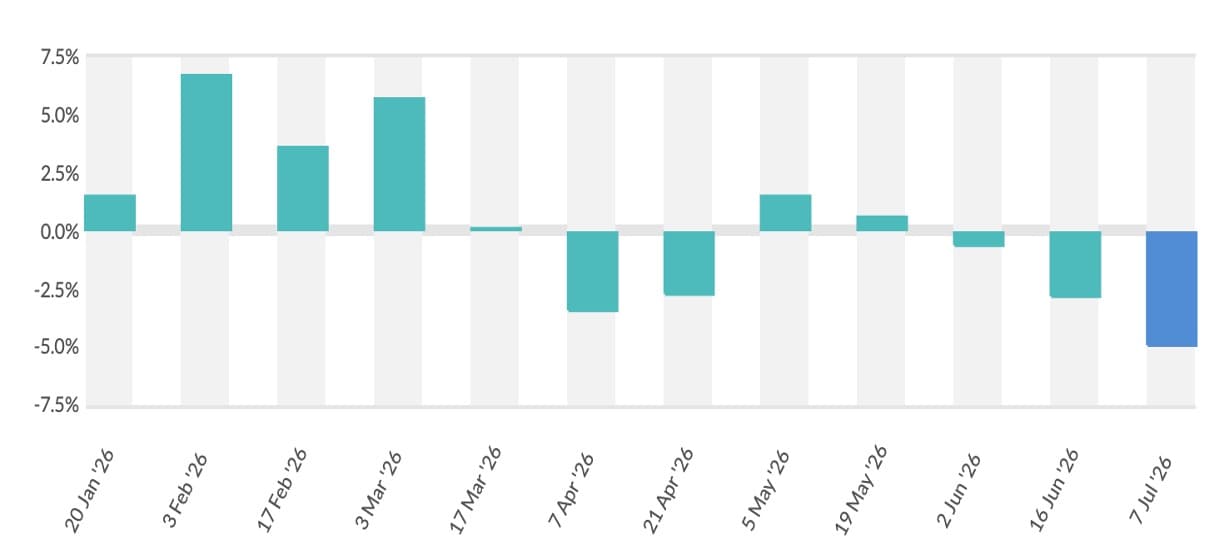

The behaviour of the GDT index since the beginning of 2026 clearly shows three distinct phases. The year started with a strong bullish rally supported by tight global supply and elevated fat prices. March and April then entered a correction phase as butter and AMF began easing. Events 403 and 404 now indicate that the market is stabilising again, but under a new leadership structure where powders rather than fats are driving sentiment. The current phase is therefore more balanced and sustainable compared to the speculative rally seen earlier in the year.

Looking ahead to the next two to three months, the market is expected to remain stable to slightly firm. WMP is likely to remain in the range of USD 3,700–3,900/MT, while SMP may continue trading between USD 3,450–3,650/MT with a firm undertone. Butter may witness intermittent recovery depending on foodservice demand and European milk production trends, whereas AMF could remain volatile and range-bound. Unless China returns aggressively to the market, the probability of another sharp rally appears limited. At the same time, controlled inventories and disciplined buying behaviour reduce the risk of any major downside collapse.

For India, the latest auction carries important strategic implications. WMP and SMP prices remaining above USD 3,500/MT improve export viability for Indian processors, especially in institutional markets and nearby regions. Opportunities are emerging in SMP, dairy ingredients and fat-filled powder categories. However, India’s domestic milk cycle remains structurally tight due to supply-side constraints and firm procurement prices. Therefore, despite moderation in some global fat commodities, Indian dairy prices are unlikely to soften significantly in the near term.

Overall, Event 404 reinforces that the global dairy market is transitioning from a speculative fat-driven rally towards a more disciplined, powder-supported and geographically diversified growth phase. The market today is not aggressively bullish, but it is considerably more stable, balanced and demand-supported than it was at the beginning of the year.

Source :Dairynews7x7 May 19th 2026 GDT event 404 review by Kuldeep Sharma

Stay Updated

Get the latest dairy industry news directly in your feed.