Latest Blogs

See More

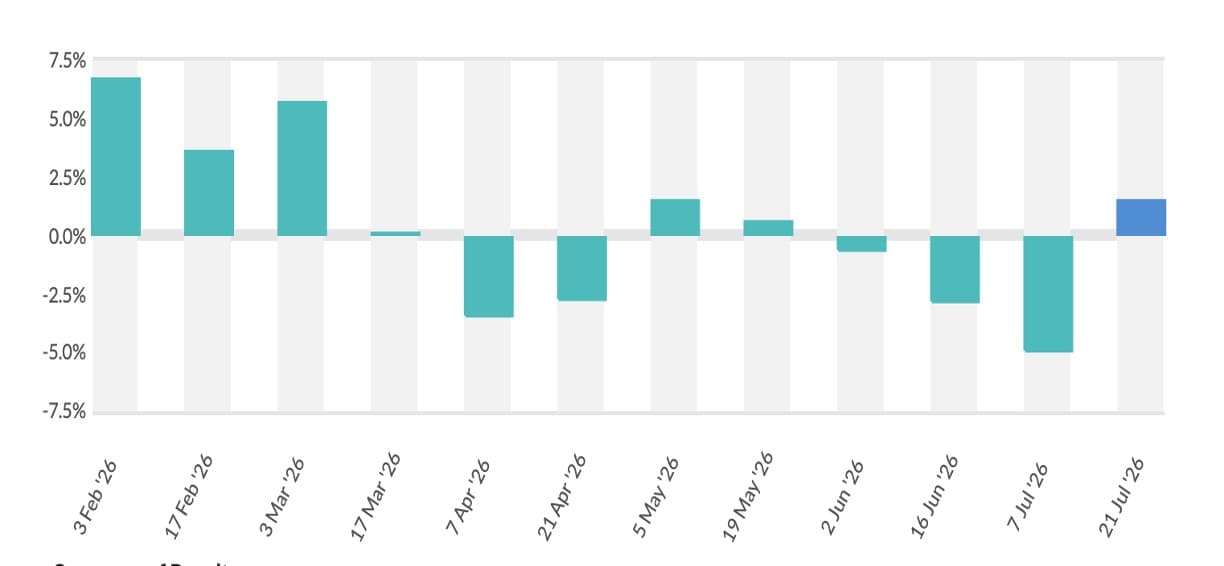

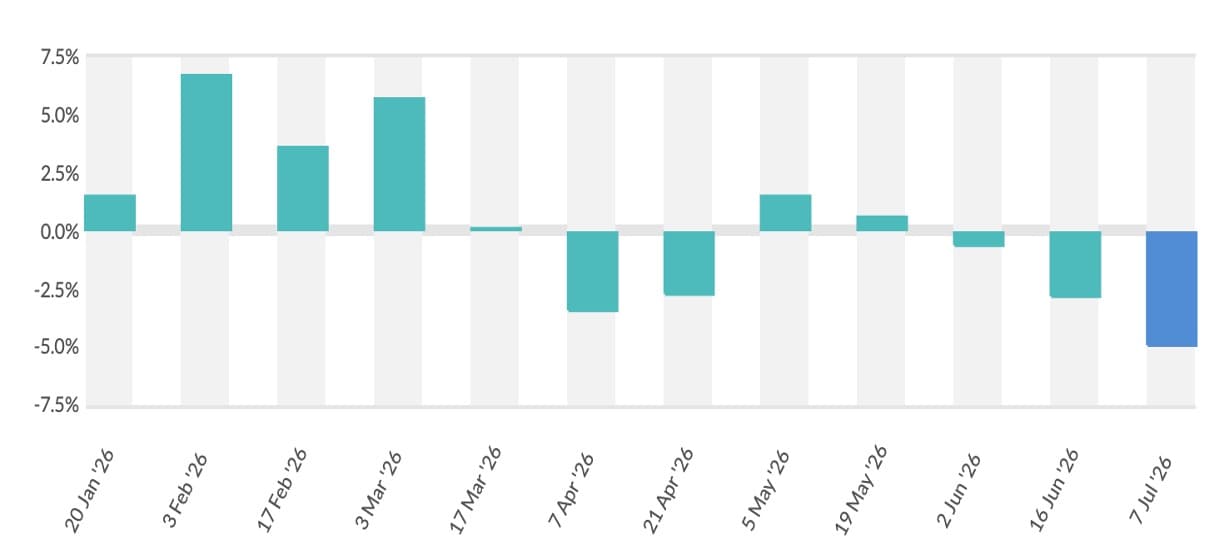

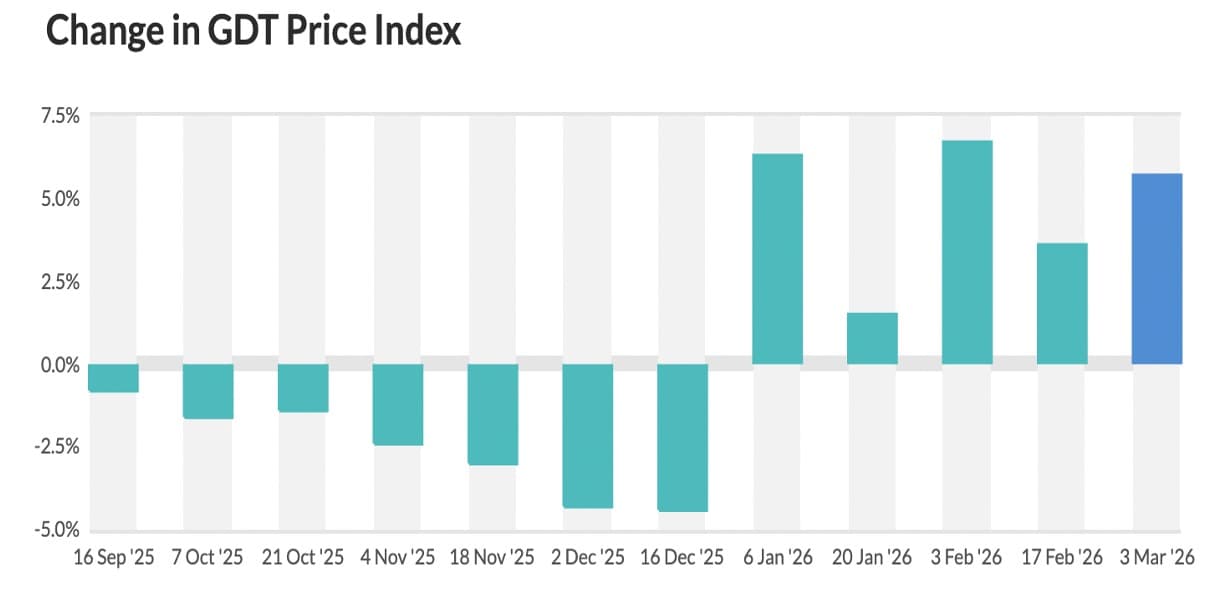

The latest Global Dairy Trade (GDT) Event 399 held on 3 March 2026 delivered a strong market signal, posting a 5.7 % rise in the GDT Price Index, with the overall average price reaching USD 4,301 per tonne amid robust buyer participation and firm bidding across key commodities. This marked the fifth consecutive auction increase, reinforcing a recovery trend from the deep price slump of late 2025 that followed unprecedented global oversupply and stock accumulation in developed markets.

At the March 3 auction, 165 bidders participated and 97 were successful over 18 rounds of trading, with total transaction volumes around 18,861 t — indicating a healthy level of market activity even as available offer volumes remained more constrained. The index gain was broad-based: **skim milk powder led with a 9.1 % jump, followed by strong advances in butter (6.1 %), anhydrous milkfat (5.7 %), whole milk powder (4.5 %) and cheese (cheddar 4.3 %, mozzarella 7.9 %). Only niche categories such as lactose (-3.9 %) and buttermilk powder (-0.2 %) saw softer pricing.

The price rebound at GDT 399 comes even as global dairy markets have struggled with high stocks and a late-cycle oversupply in 2025, which once dragged commodity values sharply lower. Several factors are now supporting the shift:

• Seasonal supply adjustments: Major exporting regions, especially Oceania (New Zealand), are moving past peak milking seasons, reducing offer volumes and partly tightening available powder supplies.

• Strong buying interest: Importers in North and South Asia, Europe, Middle East and Africa are active buyers, absorbing available products amid tighter home inventories and diversified sourcing, particularly in core use categories such as milk powders and butter.

• Inventory discipline: Buyers increasingly report “buying what they need rather than stocking large quantities,” reflecting wary restocking amid price uncertainty, which limits downward pressure on prices despite earlier large global stocks.

• Futures & hedging interest: At the CME Group futures market, dairy derivatives are experiencing record open interest and volume, signalling strong risk management activity and investor confidence in sustained prices. Tightening nonfat dry milk and butter inventories along with robust demand for whey products have driven risk hedging activity.

On the demand side, growth is no longer confined to traditional import markets. Middle East, Africa and intra-Asia regions are showing expanding participation at auctions, with Middle Eastern buyers notably strengthening their purchase share despite geopolitical logistics challenges. Additionally, domestic demand in the United States and emerging Asian markets for proteins and value-added dairy ingredients is absorbing more locally produced milk solids, which supports export demand indirectly.

Global geopolitical tensions — particularly those affecting shipping lanes near the Strait of Hormuz — are increasingly factored into dairy trade dynamics. Disruptions in freight routes and risk-adjusted logistics costs can tighten physical availability in destination markets, prompting buyers to secure tonnage ahead of potential supply chain hiccups. This dynamic, coupled with heightened risk premiums, has played a role in dampening offer volumes at GDT auctions and supporting stronger bidding.

Forecast (2–3 months):

In the near term, GDT prices are likely to remain firm or moderately higher if seasonal supply adjustments continue and buyers maintain disciplined restocking patterns. If demand from Asia and the Middle East holds or expands — especially in value-added ingredients and protein segments — price upside remains possible. However, if supply from Northern Hemisphere producers rises later in the season, the pace of increases may moderate.

Looking medium-term, sustained tensions affecting shipping and logistics near key geopolitical choke points (e.g., Hormuz) could keep exporters and importers cautious, which would support pricing by limiting freely traded volumes. Conversely, any resolution or logistics easing could ease cost premiums and slow auction price gains. Overall, heightened demand diversity, ongoing restocking and supply adjustments suggest further mild price increases or stabilisation at elevated levels through mid-2026.

Source : Dairynews7x7 March 4th 2026 GDT auctions

#GDT399 #GlobalDairyPrices #MilkPowder #Butter #AnhydrousMilkFat #Cheese #DemandMomentum #GeopoliticsImpact #DairyForecast