GDT 407: Global dairy market enters correction mode

GDT 407: Global dairy market enters correction mode

The latest Global Dairy Trade (GDT) Event 407, held on 7 July 2026, has delivered the sharpest correction witnessed in the global dairy market this year. The GDT Price Index declined by 4.9%, while the average winning price fell to USD 3,793/MT, reflecting broad-based weakness across major dairy commodities. Unlike the previous auction, where the correction was moderate and largely confined to powders, Event 407 witnessed a sharp pullback in both milk powders and milk fats, indicating that global buyers are adopting a wait-and-watch approach amid improving milk availability and subdued purchasing sentiment. The auction attracted 148 participating bidders, of which 111 emerged as winning bidders. The trading lasted 2 hours and 46 minutes, with 26,316 MT of dairy products sold against an offered quantity ranging between 25,081 MT and 30,737 MT.The most significant pressure was visible in the powder segment, which continues to dictate global dairy trade. Whole Milk Powder (WMP), accounting for nearly half of the traded volume on the GDT platform, declined by 4.4% to USD 3,425/MT, while Skim Milk Powder (SMP) registered an even steeper decline of 7.0% to USD 3,135/MT. The sharp fall in SMP suggests weakening buying interest from industrial users and importers who have largely completed their immediate replenishment. WMP also lost momentum as buyers across Asia preferred to postpone fresh purchases in anticipation of lower prices in the coming auctions.

The milk fat complex also remained under pressure. Butter declined by 5.0% to USD 5,336/MT, while Anhydrous Milk Fat (AMF) fell by 3.9% to USD 6,341/MT. This correction indicates that the premium enjoyed by milk fats during the first quarter of 2026 is gradually eroding as milk production improves in Oceania and Europe. Buyers are no longer chasing supplies aggressively and are instead purchasing only against confirmed requirements. Although butter and AMF continue to command historically healthy prices, the market is clearly moving away from the supply-driven rally witnessed earlier this year.

The cheese market also reflected divergent trends. Cheddar recorded the steepest fall among all major commodities, declining by 12.3% to USD 3,900/MT, suggesting weak foodservice demand and improved export availability from Western suppliers. In contrast, Mozzarella increased by 3.8% to USD 3,897/MT, supported by steady demand from quick-service restaurants and pizza manufacturers, particularly in Asia and the Middle East.

Among specialty ingredients, Butter Milk Powder (BMP) emerged as the best performer, rising 8.2% to USD 3,786/MT, indicating sustained demand from recombination and processed food industries. Lactose, however, declined by 3.6% to USD 1,732/MT, suggesting some moderation in demand from nutrition and pharmaceutical applications after several auctions of steady gains.

The broad correction witnessed in Event 407 is primarily demand-driven rather than supply-led. Importers across key dairy-consuming regions are becoming increasingly cautious amid global economic uncertainties, currency volatility and easing inflation. China continues to remain a disciplined buyer, purchasing only according to short-term consumption requirements rather than rebuilding inventories. The country is no longer acting as the single driver of global dairy prices, as was the case during previous dairy cycles.

Encouragingly, demand is becoming geographically more diversified. Countries across Southeast Asia, the Middle East, North Africa and Sub-Saharan Africa continue to import significant volumes of milk powders for recombination, confectionery, bakery and nutritional applications. These emerging demand centres are providing a degree of stability to the global dairy market, even though they are not yet large enough to fully offset weaker buying from China. Consequently, the current market can best be described as one of steady underlying demand but cautious procurement behaviour.

From the perspective of developed dairy-exporting regions, the correction reflects improving seasonal milk availability in New Zealand, steady production in Europe, and comfortable inventories in the United States. As supply constraints ease, buyers have gained greater negotiating power, resulting in softer prices across most dairy commodities. The decline is therefore more reflective of improving market balance than of any structural weakness in dairy consumption.

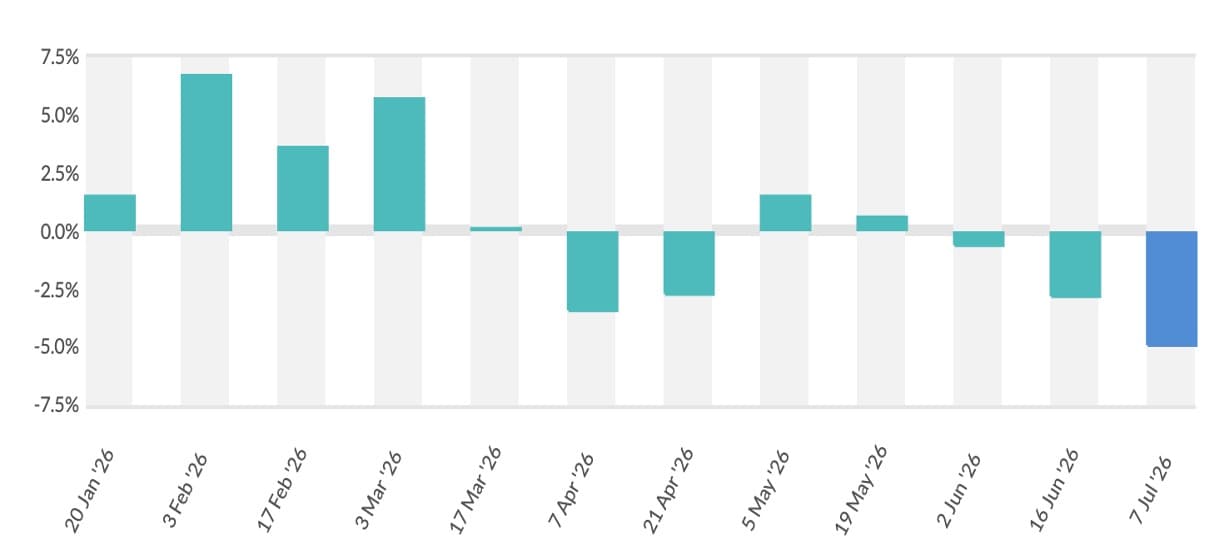

Looking at the performance of the GDT index since the beginning of 2026, the market has moved through four distinct phases. January and early February witnessed a strong rally supported by tight milk supplies and exceptionally firm milk fat prices. March marked the peak of optimism before the market entered a gradual correction during April. Events 403 and 404 briefly suggested stabilisation, while Events 405 and 406 signalled renewed weakness in powders. Event 407 has now confirmed that the global dairy market has entered a clear correction phase, with prices adjusting across almost every major product category.

Over the next two to three months, global dairy prices are likely to remain under pressure, although the pace of decline may moderate. Whole Milk Powder is expected to trade in the range of USD 3,300–3,500/MT, while Skim Milk Powder may remain between USD 3,000 and USD 3,250/MT. Butter is likely to stabilise around USD 5,200–5,500/MT, whereas AMF could fluctuate between USD 6,200 and USD 6,500/MT. Any significant recovery would depend on stronger import demand from China, weather-related supply disruptions in Oceania or a faster-than-expected improvement in global foodservice demand.

For India, Event 407 carries important implications. The sharp fall in international SMP prices to USD 3,135/MT narrows export opportunities for Indian manufacturers unless domestic milk prices soften. However, lower international prices could improve the competitiveness of dairy ingredient imports for specialised food manufacturers where permitted. The correction in butter and AMF prices is also unlikely to significantly impact India's domestic ghee market, as domestic demand continues to remain robust and milk procurement prices are still relatively firm. Indian dairy companies will therefore continue to derive their growth largely from domestic consumption rather than exports.

Overall, GDT Event 407 marks the most decisive correction in global dairy markets during 2026. While the decline may appear sharp, it represents a healthy rebalancing after an exceptionally strong start to the year. Demand remains visible but increasingly price-sensitive, supply is improving across major exporting nations, and buyers are purchasing more strategically. The coming auctions will determine whether this correction finds a floor or evolves into a more prolonged period of softer global dairy prices.

Review article on GDT Event 407 result by Kuldeep Sharma Chief Editor Dairynews7x7