Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

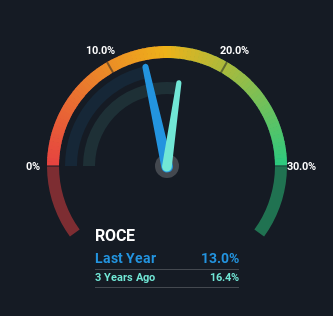

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Firstly, we’ll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. However, after briefly looking over the numbers, we don’t think Dodla Dairy has the makings of a multi-bagger going forward, but let’s have a look at why that may be.

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

0.13 = ₹1.3b ÷ (₹13b – ₹2.2b) (Based on the trailing twelve months to March 2023).

Therefore, Dodla Dairy has an ROCE of 13%. In absolute terms, that’s a pretty normal return, and it’s somewhat close to the Food industry average of 12%.

On a side note, Dodla Dairy has done well to pay down its current liabilities to 17% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Some would claim this reduces the business’ efficiency at generating ROCE since it is now funding more of the operations with its own money.

While Dodla Dairy doesn’t shine too bright in this respect, it’s still worth seeing if the company is trading at attractive prices.

While Dodla Dairy may not currently earn the highest returns, we’ve compiled a list of companies that currently earn more than 25% return on equity.