Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

FY25 is expected to see an accelerated double-digit growth for DDL, thanks to a pick-up in domestic milk volumes, commencement of a new plant in Kenya, and a massive increase in cattle feed capacity

Milk procurement prices are projected to remain stable this fiscal year, thanks to steady input costs. Combined with enhanced operating efficiencies and a greater focus on value-added products, this stability is expected to support strong double-digit margins for DDL.

With a solid balance sheet and strong cash flow generation, DDL is well-positioned to explore inorganic growth opportunities.

DDL stands out as one of the few high-quality listed dairy companies, boasting a track record of industry outperformance, a reputable brand, and an experienced management team. Since our recommendation in October 2023, the stock has delivered a robust 44% return, compared to the Nifty 500 index's 25% return in the same period. We maintain our positive outlook on the stock.

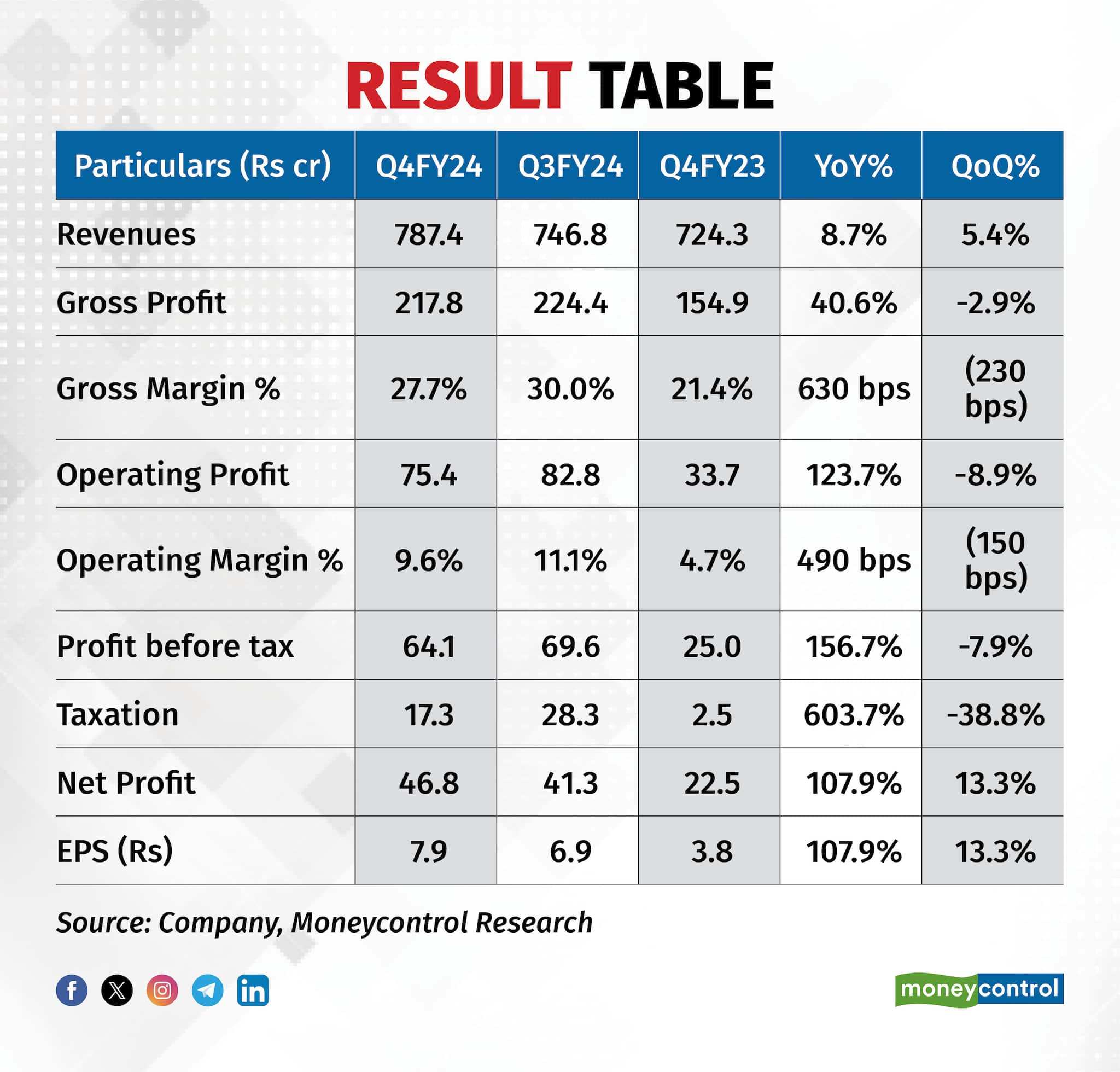

Gross margins improved by approximately 600 bps YoY, benefiting from lower raw material prices during the flush season and higher VAP sales. DDL recorded an inventory write-down of about Rs 23 crore in Q4FY24 to reflect the net realizable value.

Excluding the write-down, gross margins would have been about 300 bps higher. EBITDA margins improved by 490 bps, slightly less due to increased employee and advertising expenses after commissioning new plants. Net profits more than doubled YoY.

In Q4FY24, DDL started its new dairy plant in Kenya, Africa, with a capacity of 1 lakh liters per day, which will drive growth momentum. Additionally, DDL increased its Orgafeed (cattle feed) capacity five-fold to 480 MTPD (metric tonnes per day) last fiscal year, which will further boost growth. DDL plans to liquidate the inventory built up towards the end of the last fiscal year, primarily fat and milk powder, as inventory days increased from 15 days in FY23 to about 45 days in FY24.