Latest Blogs

See More

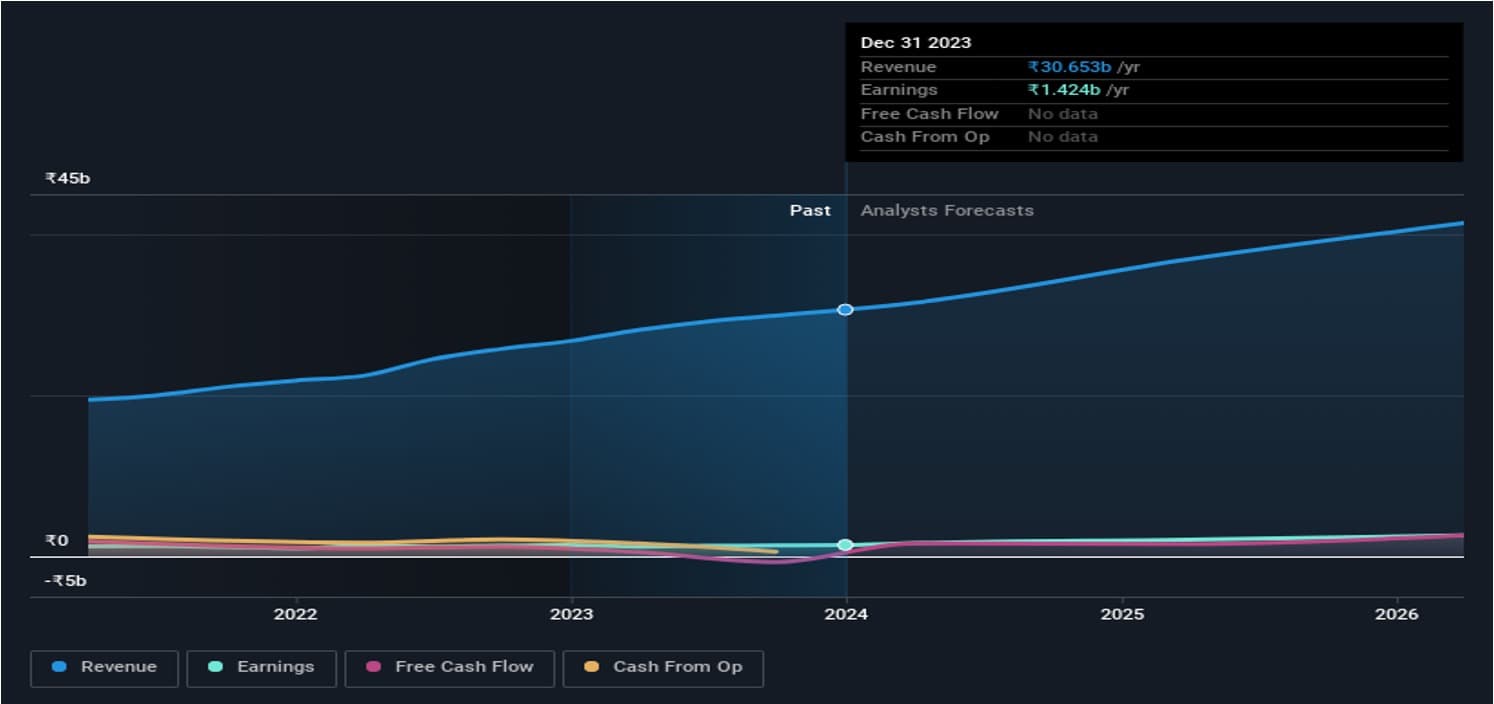

Dodla Dairy Limited (NSE:DODLA) just released its latest third-quarter report and things are not looking great. Dodla Dairy missed earnings this time around, with ₹7.5b revenue coming in 3.1% below what the analysts had modelled. Statutory earnings per share (EPS) of ₹6.88 also fell short of expectations by 15%. Earnings are an important time for investors, as they can track a company’s performance, look at what the analysts are forecasting for next year, and see if there’s been a change in sentiment towards the company. We’ve gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Taking into account the latest results, the current consensus from Dodla Dairy’s three analysts is for revenues of ₹36.9b in 2025. This would reflect a huge 20% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to surge 48% to ₹34.95. In the lead-up to this report, the analysts had been modelling revenues of ₹37.1b and earnings per share (EPS) of ₹35.15 in 2025. The consensus analysts don’t seem to have seen anything in these results that would have changed their view on the business, given there’s been no major change to their estimates.

With the analysts reconfirming their revenue and earnings forecasts, it’s surprising to see that the price target rose 12% to ₹868. It looks as though they previously had some doubts over whether the business would live up to their expectations. That’s not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Dodla Dairy analyst has a price target of ₹920 per share, while the most pessimistic values it at ₹815. This is a very narrow spread of estimates, implying either that Dodla Dairy is an easy company to value, or – more likely – the analysts are relying heavily on some key assumptions.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It’s clear from the latest estimates that Dodla Dairy’s rate of growth is expected to accelerate meaningfully, with the forecast 16% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 12% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 10% annually. Factoring in the forecast acceleration in revenue, it’s pretty clear that Dodla Dairy is expected to grow much faster than its industry.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider.