Latest Blogs

See More

Another primary reason is the decline in cattle numbers. Fewer animals means less milk production capability. This decrease may be linked to various factors, including excellent culling rates, disease outbreaks, and the cost of keeping a big herd. With fewer cows to milk, it’s hardly surprising that output growth has been uneven.

Increased feed prices have had a substantial impact on costs. Feed accounts for a significant amount of dairy production expenditures. When feed prices skyrocket, farmers often find themselves in a difficult situation. To minimize expenses, they may need to reduce animal nutrition, which would influence milk output. This financial hardship causes an irregular feed supply loop, resulting in variable milk.

Combining these factors—unpredictable weather, fewer cattle, and high feed costs—makes it easy to understand why global milk output has been so volatile. These elements add to a complicated narrative that affects market dynamics, pricing, and, ultimately, the supply chain. Understanding the interaction of these difficulties allows us to forecast future trends and change our strategy appropriately.

As milk prices recover, producers are more motivated to maximize output. This economic increase may help balance past obstacles, such as high feed prices and inclement weather. Farmers may feed their cattle better as feed becomes more available and inexpensive, which is expected to increase milk output.

Combining higher milk prices and lower feed costs generates a more favorable environment for increasing milk production. Rabobank believes that these circumstances will help steady, and even slightly enhance, milk output across significant areas.

Are you seeing similar patterns in your area? If so, it may be time to consider how these more significant market trends may affect your business.

On the environmental front, the expected return of La Niña weather patterns later this year adds complexity. La Niña causes more relaxed and moist weather in the Northern Hemisphere and drier conditions in the Tropics. This might be difficult for major milk-producing countries like New Zealand and Australia. Drier weather may damage pasture growth, resulting in more significant feed expenditures and, perhaps, lower milk output. In contrast, locations such as the United States Pacific Northwest may benefit from increasing precipitation, possibly improving feed and water availability for dairy cows.

Given these considerations, the confluence of geopolitical instability and climatic unpredictability emphasizes the need for strategic planning and adaptation in the dairy business. Are your operations and supply chains able to endure these disruptions? Now may be the time to examine and make any required changes.

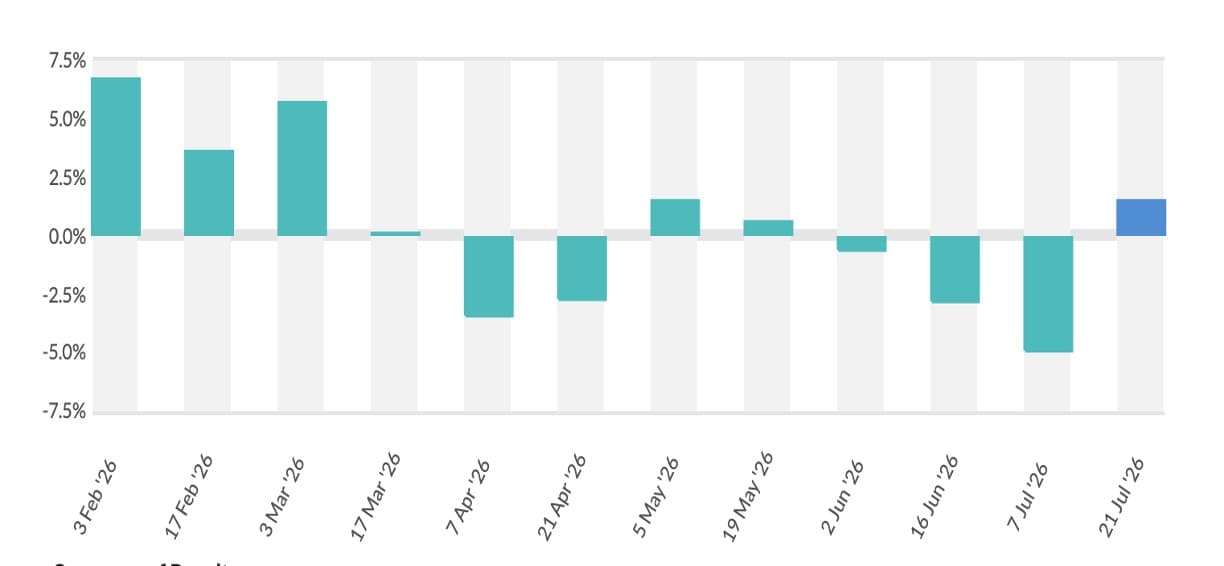

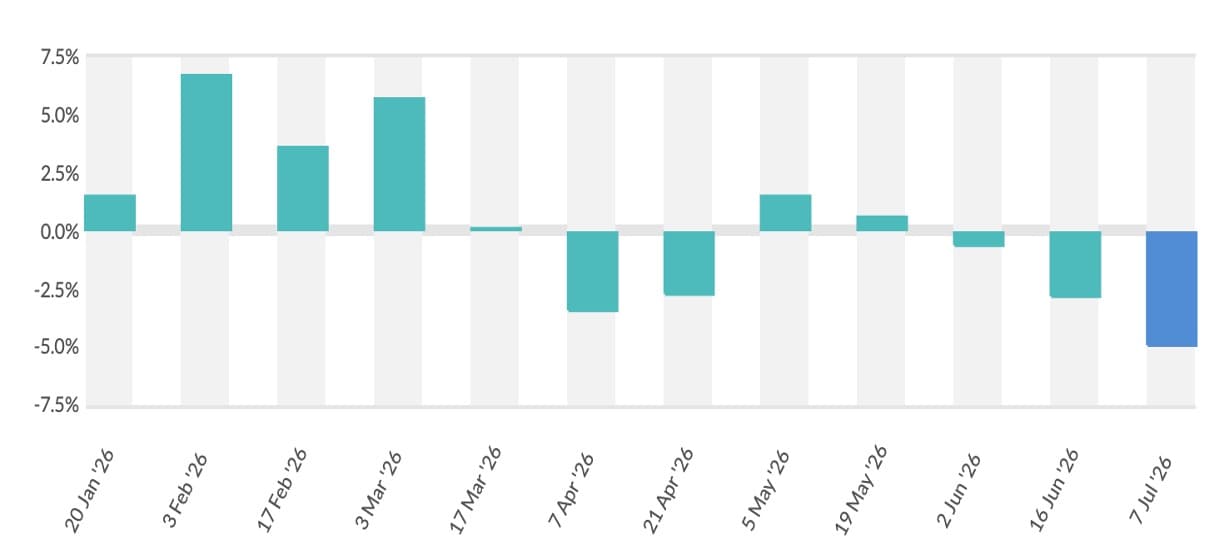

For example, milk output in the Netherlands fell by 1.9% in June. This drop highlights a challenging year for Dutch farmers. Meanwhile, Denmark and Germany showed resilience by eradicating their year-on-year milk deficits in the second quarter.

A rainy spring in Ireland created harsh circumstances, reducing milk output. The results show an 8.7% fall in the first quarter and an additional 4.2% drop in the second quarter compared to the previous year. This highlights how weather patterns may significantly affect agricultural production.

On the plus side, Poland’s milk output increased by 4.1% in May, showing significant growth. Italy and Spain also saw good trends, with outputs of 1.4% and 1.5%, respectively. These advances stand out against the backdrop of uneven outcomes.

France, the EU’s second-largest milk-producing nation, had its first year-over-year gain (0.4%) in recent years. However, this expansion has been unstable, with recent weeks indicating a decline. This variation reflects the sector’s persistent uncertainty and problems.

Overall, the European dairy market’s fragmented production patterns reflect the complex interaction of local factors and more significant economic pressures. Dairy farmers and industry partners must continue negotiating these diverse environments to achieve sustainable development.

Rabobank experts point to this slowdown after many years of solid growth. What are the reasons? Rising production costs and environmental sustainability requirements put pressure on Chinese dairy producers. This scenario is concerning, particularly for stakeholders that rely on China’s rapid expansion.

China’s anti-subsidy investigation into US dairy imports complicates matters even more. This investigation seeks to determine if American manufacturers obtain improper government subsidies, giving them a pricing edge in the Chinese market. If China imposes tariffs or other trade obstacles, the global dairy trade dynamics may change dramatically.

The United States, a major supplier to China, may see its access to this lucrative market curtailed. As a result, American dairy producers may confront an oversupply, which might lead to domestic price declines. Simultaneously, China may seek other suppliers, which might help other foreign firms while upsetting traditional supply networks.

Navigating these developments demands both alertness and agility. Are your plans adaptable enough to handle these anticipated market shifts? Staying educated and adaptive might be the difference between flourishing and surviving in an ever-changing market.

Bluetongue is already spreading across Europe, posing a danger to milk supply. What does this mean to you? If the illness is not controlled, sick cows will produce less milk, reducing the total supply and perhaps raising costs.

Let’s look at the particular examples in the EU. Italy, Poland, and Spain have all demonstrated favorable production trends, but a massive bluetongue epidemic might jeopardize these advances. The price of disease care and lower milk output might make 2024 a challenging year for European dairies.

Given Rabobank’s cautious estimates, it is critical to remain updated about this problem. Monitoring local epidemics and implementing preventative actions may help limit the hazards. After all, ensuring herd health is closely related to sustaining healthy milk output.

Furthermore, the supply side has limits. Farmers are often forced to change their feed blends due to rising feed prices, which might affect the butterfat percentage of their milk. Unpredictable weather patterns like La Niña may also affect milk production and composition.

Geopolitical instability is another critical element, especially in countries such as the Middle East. This uncertainty may disrupt supply chains, making it more difficult for manufacturers to bring their goods to market, reducing supply and keeping prices high.

But what does this imply for the dairy industry? Increased butterfat pricing might have conflicting results. Higher pricing may boost profits for makers of butterfat-rich items, but they might squeeze consumers and lower demand in the long run. Furthermore, processors that need butterfat as an input may suffer higher operating expenses, which might spread across the supply chain.

Finally, the variables that drive short-term butterfat pricing seem to create a complicated picture. Understanding these dynamics is critical for anybody working in the dairy sector, from farmers to market analysts. What tactics do you intend to use to manage this challenging market?

Keeping up with these changing storylines is critical. The dynamics outlined here have a considerable influence on your operations. Understanding these patterns allows you to make more strategic choices, such as altering manufacturing processes, entering new markets, or just keeping ahead of the curve. In a volatile business like dairy, being proactive rather than reactive may mean all the difference.